In a new study published in The Journal of Finance and Data Science, a researcher from the International School of Business at HAN University of Applied Sciences in the Netherlands introduced the topological tail dependence theory—a new methodology for predicting stock market volatility in times of turbulence.

“The research bridges the gap between the abstract field of topology and the practical world of finance. What’s truly exciting is that this merger has provided us with a powerful tool to better understand and predict stock market behavior during turbulent times,” said Hugo Gobato Souto, sole author of the study.

Enhancing Financial Forecasting with Persistent Homology

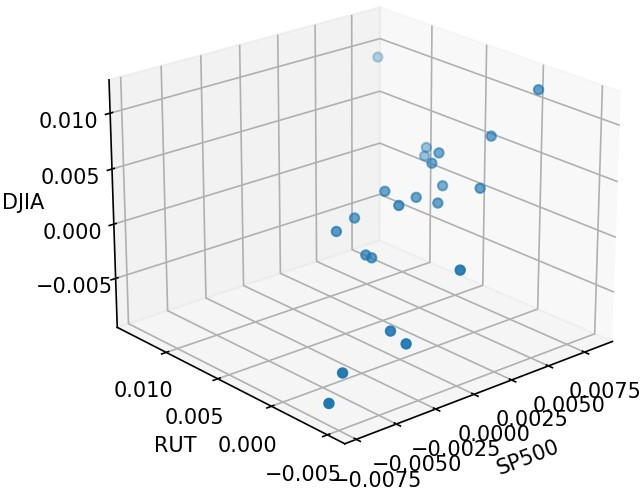

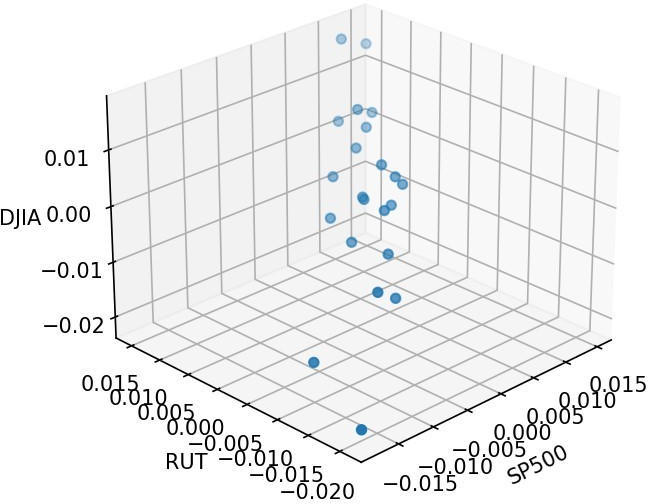

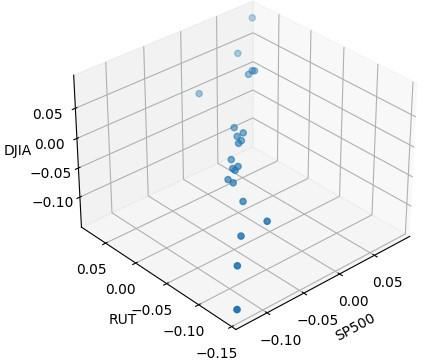

Through empirical tests, Souto demonstrated that the incorporation of persistent homology (PH) information significantly enhances the accuracy of non-linear and neural network models in forecasting stock market volatility during turbulent periods.

“These findings signal a significant shift in the world of financial forecasting, offering more reliable tools for investors, financial institutions, and economists,” added Souto.

Notably, the approach sidesteps the barrier of dimensionality, making it particularly useful for detecting complex correlations and nonlinear patterns that often elude conventional methods.

“It was fascinating to observe the consistent improvements in forecasting accuracy, particularly during the 2020 crisis,” said Souto.

Broad Implications and Future Directions

The findings are not confined to one specific type of model. It spans across various models, from linear to non-linear, and even advanced neural network models. These findings open the door to improved financial forecasting across the board.

“The findings confirm the theory’s validity and encourage the scientific community to delve deeper into this exciting new intersection of mathematics and finance,” concluded Souto.

Reference: “Topological tail dependence: Evidence from forecasting realized volatility” by Hugo Gobato Souto, 14 October 2023, The Journal of Finance and Data Science.

DOI: 10.1016/j.jfds.2023.100107

Never miss a breakthrough: Join the SciTechDaily newsletter.

Follow us on Google and Google News.

1 Comment

These people were good to me at first, but later they cheated me. In total, I was scammed out of nearly 55,000 euros. The first contact was with the administrator of the platform. He contacted me, cheated me and convinced me to make more and more deposits. I knew all the time that something was wrong, but he kept telling me to relax, that he had everything under control, and in reality he lied to me all the time. Eventually he made up the story that he had been in a serious accident and was in the hospital. When he got out of the hospital, he was replaced by another administrative assistant, who of course told the same story in a different scenario. We worked for two months when he again asked to invest a package of 15,000 euros with the intention that the bill would not die and I panicked and paid only because of the money we had invested. It took a week and he asked for another 7,000 euros to stabilize the account, to which we disagreed, and I asked him to return the money. He openly refused and laughed at me. It took me months of searching, but finally I found the solution of a expert who got back all my money, Feel free to reach to (jimbianco189 @ gmail. com) If you have the same issue, I only filed a complaint and got my money back within 2 weeks