The end of the month is here again and, with it, the credit card bill. It’s higher than you thought it would be, and you can’t even remember making some of those purchases. It’s not like you’re made of money, so why do you keep spending like this?

What is the cashless effect?

The cashless effect describes our increased willingness to buy products and to pay more for them when no physical money changes hands.

The seminal study

The cashless effect was first studied in 1979 by Elizabeth Hirschman, a prominent theorist in marketing and economics who believed that people had a tendency to spend more when they paid with a credit card rather than cash. In order to verify her suspicions, she sent field interviewers out to survey customers shopping in different branches of a department store chain.[1] They asked the customers which products they had bought and what method of payment they had used. An analysis of the data showed that people who used either a store card or a credit card made larger purchases than people who paid in cash, and that people who had both store cards and credit cards were the biggest spenders.

Hirschman concluded that people who used cashless forms of payment spent more than people who used physical money and that people who had several methods of payment available to them spent the most.

Further research has since shown that, compared to people who use cash, people who use credit cards are happy to spend more,[2] are less likely to recall their past expenditures,[3] are more likely to focus on and remember product benefits — like product quality, features, looks, the social prestige of owning the product — rather than costs,[4] and make more unplanned,[5] indulgent,[6] and unhealthy[7] purchases. The effect is similar for people who use bank cards rather than cash.[8]

How it works

Several theories have been put forward to explain the existence of the cashless effect. A controversial one is the idea of classical conditioning, suggested by economist Richard Feinberg. In 1986, Feinberg carried out four separate experiments[9] in which he led volunteers to believe that they would be evaluating products like clothing and electric typewriters. Half of the volunteers just saw pictures of the products, and half saw the same pictures accompanied by a Mastercard logo. All were asked how much they would be willing to pay for the product.

The results showed that the volunteers who were exposed to the credit card logo were more willing to buy the products, were prepared to pay more for them, and were faster to make their spending decisions. Feinberg concluded that because we associate credit cards with spending, we are more easily prompted to spend money when we use them, and that this effect is reinforced by the positive feelings that we enjoy when we spend money and buy things. The results of later research, however, have been mixed. Some studies have not been able to replicate his results,[10] and some have only partially supported them.[11]

A leading alternative hypothesis is that credit cards facilitate our buying behavior by making us feel less psychological pain when we spend physical money, reducing the so-called “pain of payment.”[12] They do this by “decoupling” (disassociating) payments from consumption[13] and allowing us to keep the cost of the item “out of mind” at the moment of purchase. One way they achieve this is by delaying the pain of payment (until the monthly bill arrives, anyway) and thus separating the pleasure of buying from the pain of paying.

However, the finding that debit cards also produce a cashless effect, even though the payments are immediately charged to your bank account, suggests that it is not so much the delaying of the payments but rather the abstract and unemotional nature of paying with a card that reduces our psychological pain. Physical money has more obvious value than a plastic card; when we spend it, we physically have to give it up, and since we have to count out our cash, the payment amount is more memorable. Cash payments leave a vivid memory trace, and the pain of payment is reinforced every time a transaction takes place. It’s much easier to part with money when it isn’t tangible.

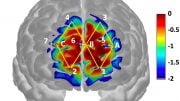

A recent fMRI study[14] provided support for both theories by revealing that buying things with credit cards activates the reward centres in our brains, and it does this regardless of the price. In contrast, when it comes to cash purchases, the rewards networks are only activated for purchases of cheaper items. The authors of the study concluded that the brain’s reward network is chronically sensitized by our prior experience with credit cards, and that exposure to credit cards and their logos may both activate the pursuit of rewarding products and alleviate the psychological pain associated with paying for them by making the price seem unimportant.

How to avoid it

The cashless effect can theoretically occur anytime we use digital forms of payment, which, as we move to cashless societies, has the potential to make overspending a rampant problem. That said, a 2021 meta-analysis of studies carried out after 2004 revealed that the cashless effect has become weaker over the years, perhaps because technological advances have made it possible for us to check our credit card balances before getting the bill, or perhaps because cashless payment methods have become so widespread that we have gotten used to spending and paying the bill later; the analgesic magic has worn off.[15]

But if you are worried that you might overspend on your credit card, making the pain of paying more salient has been shown to curb the inclination to spend. This can be done by anticipating the future pain of paying — for example, by remembering the regret you felt the last time you had to pay a large credit card bill — or by using a “decomposition strategy,”[16] which involves estimating the cost of each item in your basket individually rather than coming up with a total amount.

For example, if you are planning a large Thanksgiving meal, instead of putting all the ingredients in your basket and estimating the total cost, you estimate the cost of the turkey, cranberry sauce, gravy, stuffing, vegetables, salad dressing, breads, pies, cheese, fruit, nuts, wine, and so on, and then you add them together to get the total amount. This should make the pain of parting with money more obvious by focusing your attention on many small payments rather than one large payment. Now you can put some of that stuff back.

An alternative way of dealing with this bias is to focus on the idea that credit cards make it easy for us to overspend because they remove friction — the obstacles we must negotiate — from the payment experience. But you can replace the friction. You can make it more difficult to make unplanned purchases with your credit card by always leaving home without it. Having to rush off and find an ATM so that you can buy that cool portable projector you just saw at Best Buy may very well cool your enthusiasm. Or you can literally freeze your credit card in a block of ice and hope that it still works when you thaw it out again (tip: don’t use a microwave).

Of course, these are just band-aid solutions that don’t treat the root of the problem. The best thing you can do to reduce your credit card bill is to prevent overspending in general by, for example, creating a spending budget and making sure that you don’t spend more money than you have in your bank account, or taking a few days to consider that big purchase you’re thinking of making. The trick is to stop thinking of your credit card as a way to buy things you can’t afford to get with hard cash.

References:

- Hirschman, E. C. (1979). Differences in Consumer Purchase Behavior by Credit Card Payment System. Journal of Consumer Research, 6(1), 58-66.

DOI: 10.1086/208748 - Prelec, D., & Simester, D. (2001). Always leave home without it: A further investigation of the credit-card effect on willingness to pay. Marketing letters, 12(1), 5-12.

DOI: 10.1023/A:1008196717017 - Srivastava, J., & Raghubir, P. (2002). Debiasing using decomposition: The case of memory-based credit card expense estimates. Journal of Consumer Psychology, 12(3), 253-264.

DOI: 10.1207/S15327663JCP1203_07 - Chatterjee, P., & Rose, R. L. (2012). Do payment mechanisms change the way consumers perceive products? Journal of Consumer Research, 38(6), 1129-1139.

DOI: 10.1086/661730 - Inman, J. J., Winer, R. S., & Ferraro, R. (2009). The Interplay among Category Characteristics, Customer Characteristics, and Customer Activities on in-Store Decision Making. Journal of Marketing, 73(5), 19-29.

DOI: 10.1509/jmkg.73.5.19 - Soman, D. (2003). The Effect of Payment Transparency on Consumption: Quasi-Experiments from the Field. Marketing Letters, 14(3), 173-183.

DOI: 10.1023/A:1027444717586 - Thomas, M., Desai, K. K., & Seenivasan, S. (2011). How credit card payments increase unhealthy food purchases: visceral regulation of vices. Journal of consumer research, 38, 126- 139.

DOI: 10.1086/657331 - Runnemark, E., Hedman, J., & Xiao, X. (2015). Do consumers pay more using debit cards than cash? An experiment. Electronic Commerce Research and Applications, 14(5), 285-291.

DOI: 10.1016/j.elerap.2015.03.002 - Feinberg, R. A. (1986). Credit cards as spending facilitating stimuli: A conditioning interpretation. Journal of Consumer Research, 13(3), 348-356.

DOI: 10.1086/209074 - Hunt, J. M., Chatterjee, A., Florsheim, R. A., & Kernan, J. B. (1990). Credit Cards as Spending-Facilitating Stimuli: A Test and Extension of Feinberg’s Conditioning Hypothesis. Psychological Reports, 67(1), 323-330.

DOI: 10.2466/pr0.1990.67.1.323 - Shimp, T.A. & Moody, M. P. (2000). In Search of a Theoretical Explanation for the Credit Card Effect. Journal of Business Research, 48(1), 17-23.

DOI: 10.1016/S0148-2963(98)00071-X - Soman, D. (2001). Effects of payment mechanism on spending behavior: The role of rehearsal and immediacy of payments. Journal of Consumer Research, 27(4), 460-474.

DOI: 10.1086/319621 - Prelec, D., & Loewenstein, G. (1998). The Red and the Black: Mental accounting of savings and debt. Marketing Science, 17(1), 4-28.

DOI: 10.1287/mksc.17.1.4 - Banker, S., Dunfield, D., Huang, A., & Prelec, D. (2021). Neural mechanisms of credit card spending. Scientific Reports, 11(1), 4070.

DOI: 10.1038/s41598-021-83488-3 - Liu, Y., Dewitte, S. (2021). A replication study of the credit card effect on spending behavior and an extension to mobile payments. Journal of Retailing and Consumer Services, 60, 102472.

DOI: 10.1016/j.jretconser.2021.102472 - Raghubir, P., & Srivastava, J. (2008). Monopoly money: The effect of payment coupling and form on spending behavior. Journal of Experimental Psychology: Applied, 14(3), 213-225.

DOI: 10.1037/1076-898X.14.3.213

Every time I check my credit card balance and get surprised my first response is to ask, “was this me?”. And then undertake a spending fast even on habitual purchases. I can really live without the dubious real benefits of much I buy.